Key Takeaways

- April demonstrated how quickly investor sentiment can recover once geopolitical risks stabilise and earnings momentum returns. The rebound was not only sharp, but powerful enough to fully erase March’s drawdown across several portfolios.

- The AI infrastructure cycle continues to drive global markets, particularly across semiconductors, cloud computing, and data centre expansion. Asia’s strong market performance further reinforced its strategic importance within the global AI supply chain.

- Investors who remained disciplined during March’s volatility benefited significantly from April’s recovery. The episode once again highlighted the importance of maintaining a long-term investment approach rather than reacting to short-term market fear.

April 2026 marked one of the most remarkable reversals in recent market history. Following the sharp market collapse in March triggered by escalating US-Iran tensions, global financial markets rebounded aggressively across nearly all major asset classes.

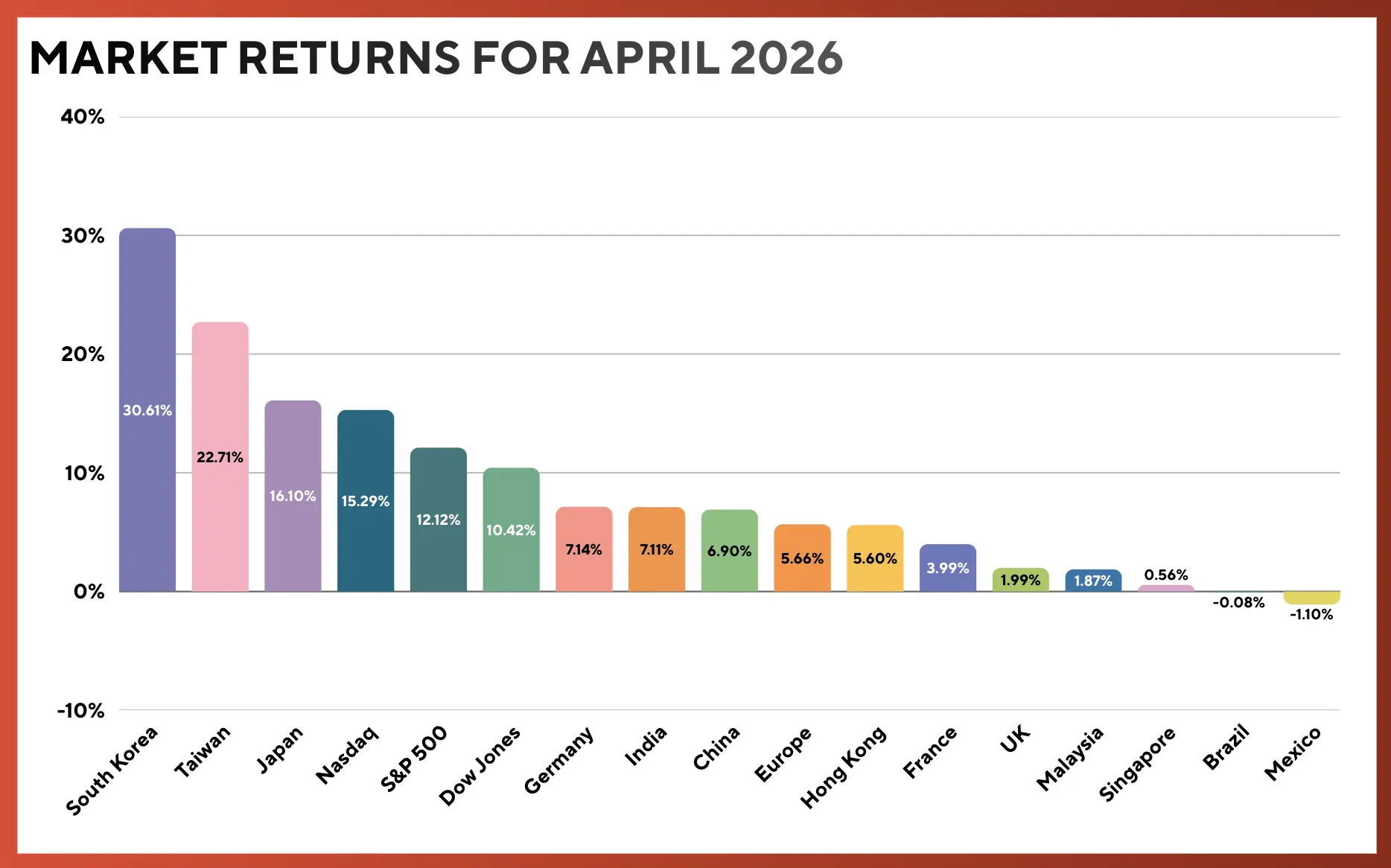

Performance of Select Markets that Monitored by Market in April 2026

**Disclaimer: Past performance is not indicative of future performance

Global equities staged a broad‑based recovery in April. The S&P 500 rose 10.42% to close at 7,209.01, marking its strongest monthly gain since November 2020, while the Dow Jones Industrial Average advanced 9.81%. The rebound was even more striking in Asia, which once again emerged as the strongest‑performing region thanks to its central role in the global semiconductor and AI supply chain. South Korea’s KOSPI Index delivered one of the most impressive performances among major markets, surging 30.61% as optimism surrounding AI‑related semiconductor demand continued to build. The sustained strength of companies such as Samsung Electronics and SK Hynix further reinforced confidence in the broader AI infrastructure theme.

Taiwan’s Weighted Index climbed 22.71%, supported by persistent demand for advanced semiconductor manufacturing led by TSMC. Japan’s Nikkei 225 also posted a solid gain of 16.10%, helped by a weaker yen and ongoing technology‑related capital expenditure.

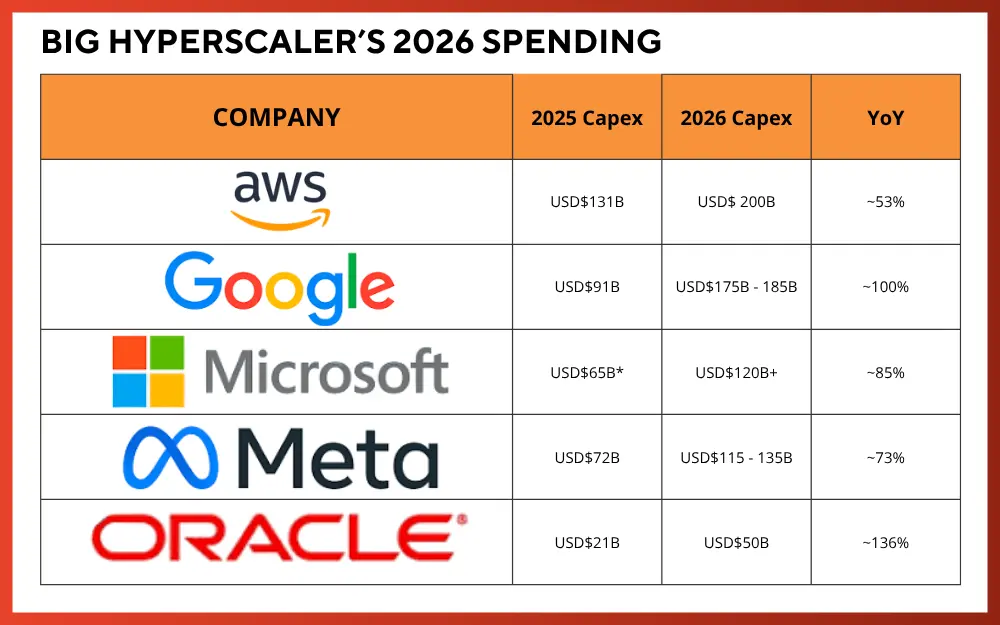

The market rebound was driven by several converging catalysts. On 8 April 2026, President Donald Trump announced a two‑week ceasefire agreement with Iran, reportedly mediated by Pakistan. This development immediately eased concerns about prolonged energy supply disruptions and restored confidence across global risk assets. At the same time, first quarter 2026 earnings significantly exceeded expectations. Large technology companies continued to show resilient earnings momentum, and major hyperscalers raised their projected AI and infrastructure spending plans. Industry estimates now suggest that AI‑related capital expenditure could approach USD 700 billion in 2026, a substantial increase from 2025.

The spending for big Hyperscalers for 2026.

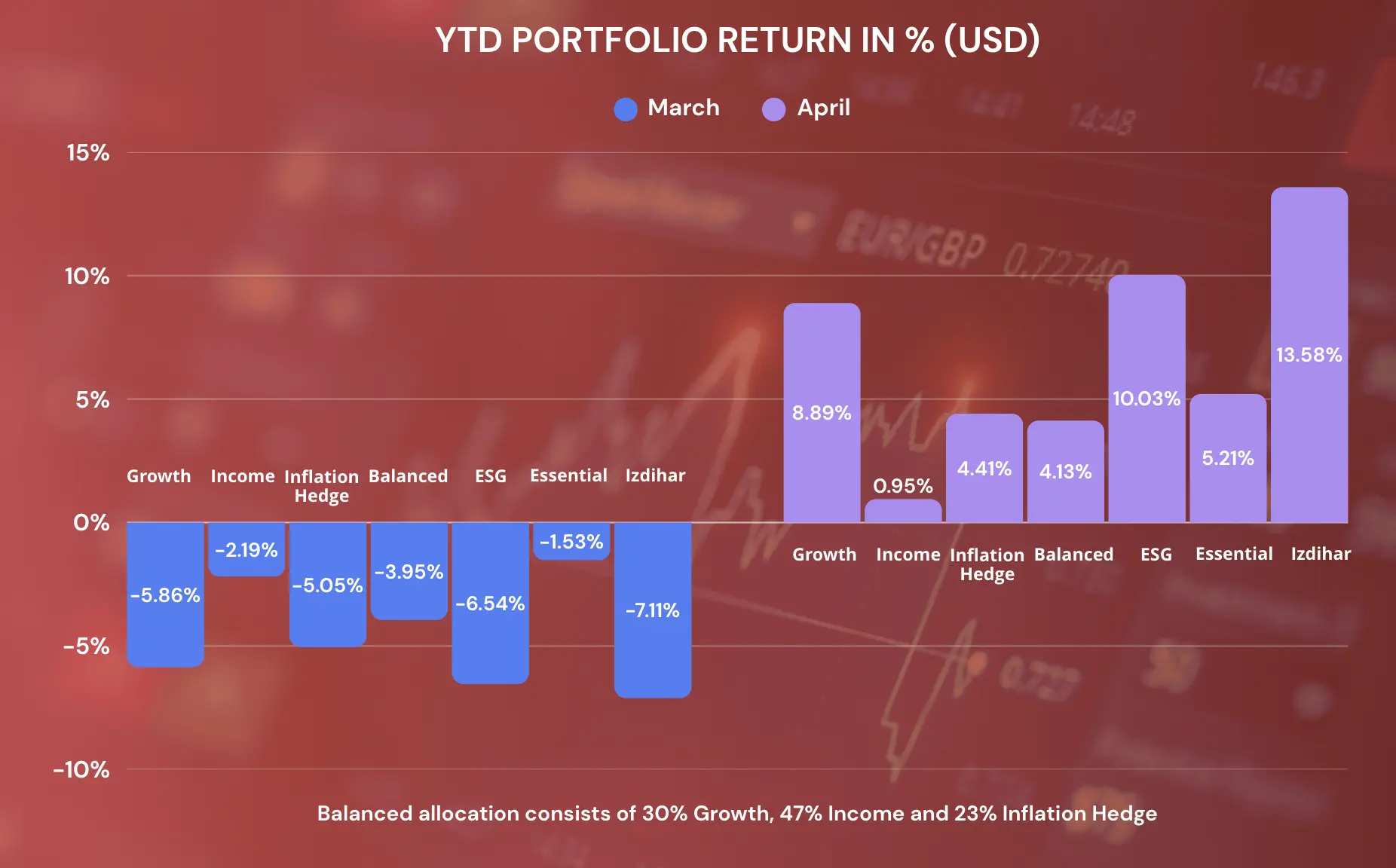

The strength of the rebound was clearly reflected across MYTHEO portfolios. The Growth, ESG, Essential, and Izdihar portfolios fully recovered the losses experienced during the March sell‑off after delivering strong gains in April. The sharp recovery in global technology and growth‑oriented equities became the primary driver of performance during the month.

Among the portfolios, MYTHEO Izdihar delivered the strongest return, gaining 13.58 % in USD terms, supported by its significant allocation to technology‑related Shariah‑compliant equities. Other equity‑oriented portfolios also performed well, with the Growth and ESG portfolios rising 8.89 % and 10.03 % respectively in just one month.

Performance of MYTHEO Portfolio for month of March and April in US Dollar

**Past performance is not an indication of future performance.

Conclusion

March was a month defined by fear. Geopolitical tensions and worries about a broader regional conflict weighed heavily on sentiment, and markets reacted accordingly. Yet within just a few weeks, the narrative shifted. As the risk of prolonged escalation eased and corporate earnings once again took centre stage, markets recovered far more quickly than many expected. What followed in April was not just a rebound, but a complete reversal that more than erased the losses suffered during the March sell‑off.

This episode is a clear reminder of how quickly market catalysts can change. In March, investors were focused on the potential disruption from the closure of the Strait of Hormuz. By April, the conversation had moved on to stronger‑than‑expected earnings and a renewed surge in AI‑related investment. The medium‑term outlook continues to be shaped by the powerful structural growth in AI infrastructure, semiconductors, and cloud computing. New headlines will inevitably emerge along the way, but markets have always evolved through cycles of fear, optimism, and innovation.

For investors, the lesson is straightforward. Looking at the big picture matters far more than reacting to short‑term noise. Those who stayed invested through the volatility were able to participate fully in April’s recovery, while those who tried to time the market risked missing the sharpest part of the rebound. Markets will continue to shift, catalysts will continue to change, and headlines will continue to come and go. What does not change is the value of staying invested with a long‑term mindset.

Consistency remains one of the most effective strategies for building wealth over time. MYTHEO’s Regular Savings Plan is designed to help investors stay disciplined through both calm and turbulent periods. You can set up your Regular Savings Plan option in the MYTHEO app or web platform, or you may contact our Customer Experience team at +6017‑673 1201 for assistance.

Ready to explore how MYTHEO works for your goals? Learn more here.

Or download our app so you can start investing in a moment. Download on iOS here or Android here.

To register for MYTHEO, you can get started here.

This material is subject to MYTHEO’s Notice and Disclaimer.